Key takeaways:

- Surgical specialists have the highest occupational disability exposure among physicians.

- As such, a quality disability insurance policy is essential for orthopedists’ financial security and asset protection.

As a coauthor of this column for a number of years now, I have covered the topic of disability insurance in the past. As all orthopedists know, in theory at least, disability can happen to any of us, and for physicians and surgeons who need to use their hands and physically examine patients, a long-term disability can be mean financial devastation if not properly protected against through insurance.

While the theory makes sense, of course, I wanted to go beyond theory in this month’s column , coauthor ed by a colleague of mine — Stephanie Pearson, MD, FACOG, an OB / GYN who suffered a long – term disability and was not protected the way she should have been. Pearson has become a physician advocate because of her experience, so I decided to use the rem a inder of this column to allow her to tell her story and educate on the topic of disability insurance, on which she has become an expert.

Source: David B. Mandell, JD, MBA, and Stephanie Pearson, MD, FACOG

I was kicked twice in the shoulder during a difficult patient delivery, had a torn labrum, developed adhesive capsulitis, had surgery and was deemed unfit to continue working as an OB/GYN. My recovery did not go as well as expected, and I have a considerable range of motion deficit and nerve damage. If you, like me, ever become unable to practice orthopedics the way you do, disability insurance can help you meet your expenses. It would allow you and your family to continue your standard of living and enable you to focus on healing, not on finances.

Stephanie Pearson

David B. Mandell

Orthopedic surgeons occupy one of the most physically demanding roles in medicine today. Your livelihoods depend on strength, dexterity, cognitive and physical endurance, and flawless motor control under conditions of fatigue and ergonomic strain. The years of training, long hours and complicated procedures leave orthopedists extremely vulnerable to injury and illness.

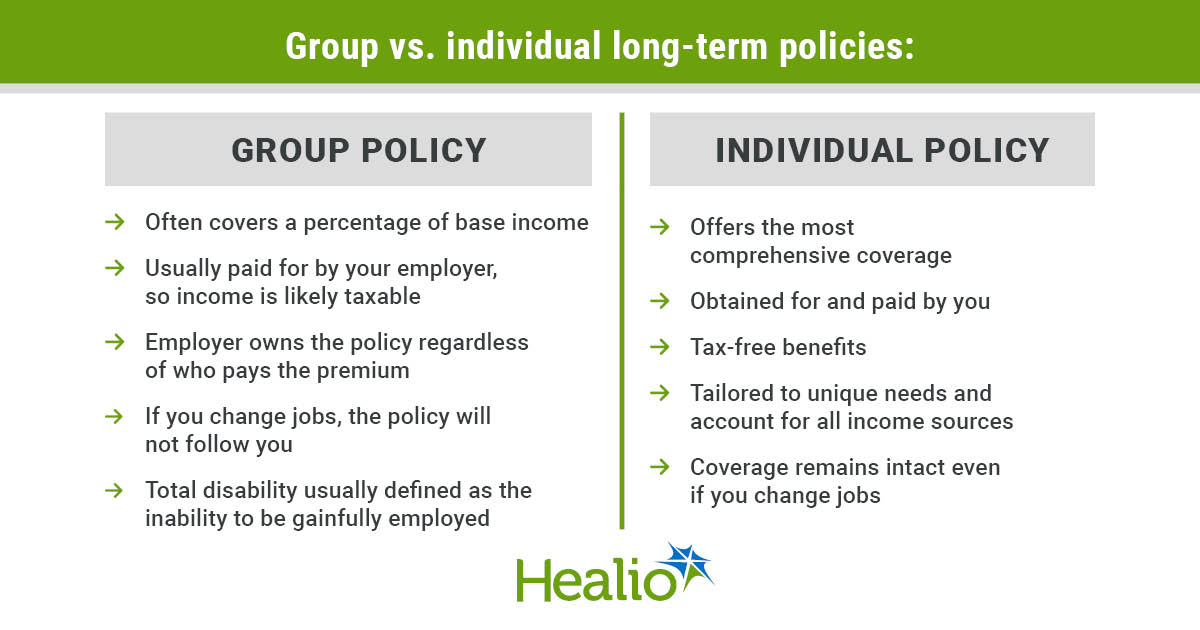

Group policy vs. individual private policy

Most group employer disability insurance benefits will only cover a percentage of your income, often your base income, and frequently up to a maximum monthly amount. An individual private disability policy will cover your entire income, up to the participation limits of the carrier.

If your employer pays for the policy, the benefits will be considered taxable. A policy that you pay for with post-tax dollars will make for a tax-free benefit.

Your employer’s policy is employment dependent. When you change jobs, it will not follow you. A private policy is portable. It is your policy throughout your career, wherever it may take you.

The language in employers’ policies is inferior to that in private policies. There are often limitations to certain claims, and the definition of own-occupation and total disability is not ideal for physicians.

How do I determine which private policy is best for me?

It is all about the riders; they are the building blocks of your policy. They lay out the benefits you stand to receive, and can be tailored to your specific, individual needs. You will want and need several riders:

- Own occupation. This goes by several different names, but it changes the language for total disability to say that you are considered totally disabled if you cannot do your job as an orthopedist, regardless of whether you are gainfully employed in another occupation. You are judged against yourself, not 100 of your peers. Carriers will look at your calendar and codes to see what makes you unique.

- Increase options. This gives you the opportunity to increase your monthly benefit without additional medical underwriting. Once you have gone through medical underwriting, you only want to share your proof of income and benefits.

- Residual/partial disability. This covers you if you have to work part-time due to injury or illness but can perform the material duties of your job. Conditions such as multiple sclerosis or other autoimmune diseases, postconcussive states and working through medical treatments are some disease processes that may not preclude you from working altogether, but they may render you unable to work long shifts. This rider closes the gap in your earnings losses.

- Cost–of–living adjustment. This rider protects against inflation when you are disabled. It will recalibrate your benefit on the anniversary of your claim.

- Catastrophic disability. This rider offers additional protection from the financial impact of a more serious injury or illness. If you need assistance with two or more of your activities of daily living, or are severely cognitively impaired, it gives you an extra benefit.

Any private policy you purchase should be automatically renewable and noncancelable. It means that if you have gone through medical underwriting, been given an offer, and paid your premiums, the carrier cannot change or cancel your policy. It is guaranteed for the duration of the policy.

An important caveat: several training institutions have a guaranteed standard issue policy offering from one or more of the traditional disability carriers. These policies require no medical underwriting; therefore, nothing is excluded from coverage. If you have underlying medical issues that would lead to exclusions or a decline, these are a great option. There are some limitations that you will want to understand. If you are a resident or fellow, make sure you look into this option.

What do orthopedists go out on claim for?

The Council for Disability Awareness and disability insurers consistently categorize surgical specialists among the physicians with the highest occupational disability exposure.

Musculoskeletal claims are one of the top reasons for all physicians leaving the practice of medicine. Ironically, surgeons who repair joints often lose their careers to joint failures. Other common disabling conditions faced by orthopedic surgeons include cervical and lumbar disc disease, rotator cuff injuries, arthritis, chronic back issues from lead aprons and surgical positioning, and repetitive stress injuries of hands and wrists. Neurological disorders, cancer, chronic pain and mental health disorders are also seen in orthopedists.

Many orthopedic surgeons maintain active lifestyles, which increases disability exposure. Accidents account for 10% to 15% of long-term disability claims. Many avocations lead to career-ending injuries, such as skiing, cycling, CrossFit and recreational sports.

Orthopedic surgeons face a distinctive occupational paradox: exceptional income potential coupled with high functional vulnerability. Securing a quality disability insurance policy is an important facet of financial planning that all orthopedists should consider as part of their asset protection plan.

For more information:

Stephanie Pearson, MD, FACOG, is a managing director and co-founder of Earned Insurance and a thought leader of the Earned Institute. She can be reached at stephanie.pearson@earned.com.

David B. Mandell, JD, MBA, is managing director at Earned and attorney and cofounder of OJM Group, an Earned company. He can be reached at 877-656-4362 or mandell@ojmgroup.com.

Mandell’s newest book is Wealth Strategies for Today’s Physician: A Multi-Media Playbook. The playbook’s innovative format features more than 90 links to videos and podcast episodes to enhance important financial topics for physicians. To receive a free print copy or ebook download, text HEALIO to 844-418-1212, or visit www.ojmbookstore.com and enter code HEALIO at checkout.

*Editor’s note: This article is for educational purposes only. Please consult a licensed financial advisor before making any investment decisions.

Sources/Disclosures

Source:

Expert Submission

References:

Disclosures:

Mandell and Pearson report no relevant financial disclosures.

Ask a clinical question and tap into Healio AI’s knowledge base.

- PubMed, enrolling/recruiting trials, guidelines

- Clinical Guidance, Healio CME, FDA news

- Healio’s exclusive daily news coverage of clinical data